The importance of pre-approval

Pre-approval….when did it become a thing? I’m not exactly sure, but like you, I was also curious. Google didn’t offer much on that exact subject, but rest assured, if you google the word “pre-approval”, you will find a myriad of information telling you just how important it is to the buying process. Now, I could just make this article short and sweet and say “get pre-approved, you’ll thank me later…” but I wouldn’t do that you guys! You’re my tribe, my peeps, my….whatever the latest hip saying is. Not only would I not leave you high and dry, but to save you the time and trouble of your own exhaustive research, I’ve done it and I’m going to delve into the subject here and give you a “one stop shopping” place to become educated. You’re welcome!

Pre-approval isn’t really as cut and dried as one would think, so it’s important to understand what it means, how it works and how to navigate the process. Wikipedia defines pre-approval as “the pre-qualification for a loan or mortgage of a certain value range”. Now to a typical consumer, the word pre-approval means that you’ve passed the approval process and are guaranteed to be granted the loan, however, the literal meaning is “at a stage before approval”. We’ve all gotten those credit card offers in the mail and in some sort of excited font, the envelope says “you’re pre-approved!”. I mean how do these companies even pretend to know enough about our financial business to just send out pre-approvals like candy thrown at a parade?

If you have already started the process of looking for a new property (be it a single family home, a condo, townhome or even commercial building) and you have talked to a real estate agent, chances are you were asked if you have been pre-approved. As an agent, I ask all of my buying clients this question. The answers vary from “yes, here is my letter” to “no, we are just starting to look” to “what do you mean?”. On the other hand, maybe you’ve only begun to think about looking, never mind even talking to an agent. Either way, this information is beneficial.

According to a recent survey by Realtor.com, of over 2,000 home shoppers who plan to purchase in the next 12 months, only 52% of them obtained pre-approval before beginning the search. This mean nearly half of home buyers are skipping this crucial step. To make it even more scary, according to the National Association of Realtors (NAR), homes are receiving an average of 2.9 offers, so bidding wars are heating up. Guys, this current market is competitive and it is a seller’s market. This mean a buyer needs to do everything they can to gain advantage over other buyers.

So, having said all of the above, the real question here is where to start. Get comfy, grab a snack and a drink. You’re not going to want to miss this!

Step One

Step One: Gather the following documents. If you’re married or going in on a property with a partner, you will both need to do this. This can take some time so I highly recommend that you don’t wait until 10 minutes before you’re scheduled to meet with a lender to start looking for everything you need….unless you’re already an organized guru and have these things at your fingertips, and if so, my hat is off to you!

Inome, financial accounts and personal information. This will include your SSN, your current address and employment details. You will also need bank and investment account info and proof of income. You will need documents such as a W-2’s and 1099’s. If you have any additional income sources, you will need to show that as well. Self-employed applicants will likely need to provide two years of income taxes.

Debts. Lenders examine your monthly debt obligations as well as your income. You will need to list all of your monthly debt payments. If you do not keep good records on your debts, you could log in to your accounts online and most likely print a statement, but if that isn’t an option then get in touch with all of the holders of these debts and request a recent statement to show where you stand with each one.

Other records.

Rent. Renters need to show payments for the past 12 months and provide landlord contact information from the past two years.

Divorce. Provide your court divorce decree and any court ordered child support and/or alimony payments made or received.

Bankruptcy and foreclosure. For this you will want to ask the lender what documents they will need.

Down payment. Lenders will want to know the sources for your down payment on the loan.

Some lenders may require additional documents or information so you may want to confirm exactly what they will look for when making the appointment.

Note…..you will want to make multiple copies of these documents, especially if you plan to visit brick and mortar lenders…..you’ll see why multiple copies are important in step two.

Step Two

Step Two: Contact a lender. Actually contact several. Shop around like you would if you were buying a car. In the United States there are literally thousands of mortgage lenders competing for your business so make them earn it. Make them be transparent about their fees, make sure they have an informative website and even a convenient online application process. You can even go so far as to research them with the Consumer Financial Protection Bureau (CFPB) to see if other borrowers have filed grievances against them. Shopping around is so important because the mortgage that one lender offers you might make your life unnecessarily challenging by wasting your money on higher rates or closing costs than another lender. Go into this with the mindset that the lenders are working for you, not the other way around, and interview them as if they were an employee you might hire to work for you.

Step Three

Step Three: This step is optional….you do not necessarily need to look all of this information up prior to interviewing lenders because they will be pulling all of the same information, however, it does not hurt to know these things about yourself. Some people keep frequent tabs on their credit score/history and others not so much. No judgement here, I’m just saying it might not hurt to know where you stand because it does directly affect the rate you are given, the type of loan you will qualify for or the ability to obtain a loan at all.

Credit score. Credit scores of at least 620 are recommended and a higher score will qualify you for better rates. A credit score of 740 or above will enable most borrowers to qualify for the best rates.

Credit history. Request copies of your credit reports, disputing any errors and if you find delinquent accounts, work with the creditors to resolve the issues. This might be especially helpful to do before talking to lenders because again, they will be looking at this and a negative credit history will impact your ability to get a decent rate or a loan at all. If you can resolve any issues in your credit history prior to applying for the loan, it may save time and money.

Calculate your debt-to-income ratio. Your DTI is the percentage of gross monthly income that goes toward debt payments. Those debt payments include such things as credit cards, student loans and car payments. You can use NerdWallet’s debt-to-income ratio calculator to help you estimate your DTI. Lenders generally prefer a DTI of 36% or below, including the mortgage you are applying for.

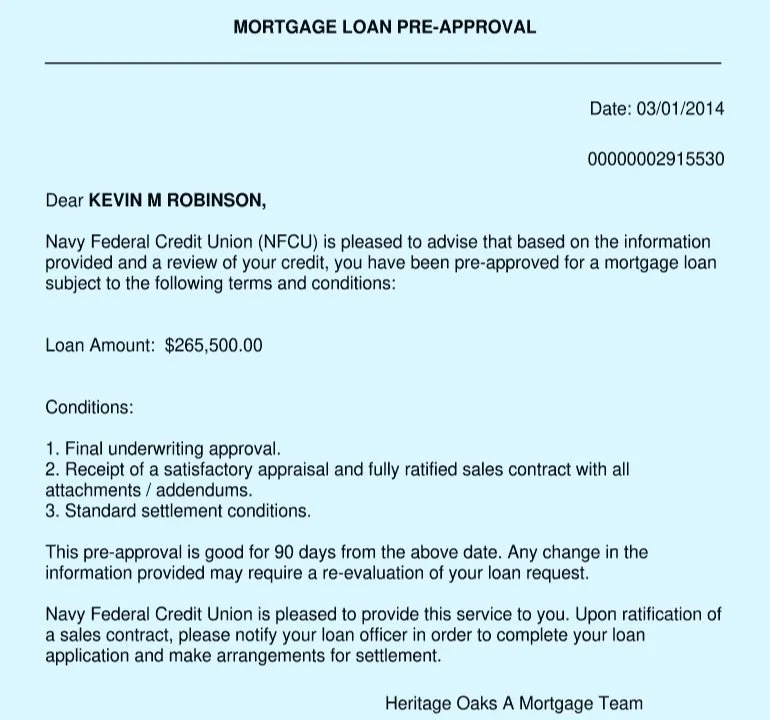

Sample pre-approval letter

So now that all of the gathering, interviewing and personal exploration is done, you’ve found a lender who fits all of your criteria and has pre-approved you for the best mortgage you can expect. It was so worth the work, right?! Right! The lender will provide you with a pre-approval letter that looks something like the above image. It should outline what they estimate you to qualify for and what the conditions of final approval are. Pre-approval letter format will vary from lender to lender of course, however they should all have the same pertinent information. Keep in mind that your pre-approval has an expiration, so, should your search for that perfect property take a while, you may need to have the lender revisit your credentials to make sure nothing has changed and then extend or renew it.

Congratulations!! Your head is now exploding with knowledge about pre-approval!! When your agent asks that all important question, you will proudly hold that letter up and shout “YES!”

Make sure to check out my other post, “Lender me your ear….” specifically speaking about Lenders. There is a LOT to weed thru when choosing a lender and by gosh I want you to be just as full with that information too!

I wish you the very, very best of luck!! I am available to answer any questions you may have, just scroll up or down and hit that “contact” button. Don’t forget to check back often and watch for other content. If there is a topic you would like to see covered, send me an email and let me know! It would make my day!